Fairfax Financial Holdings

The rebirth of a strong compounder

Fairfax Financial Holdings (FFH)

Description

Price (USD): 550

Shares Outstanding: 23,9M

BV/Share: $631

LTM P/E: 4.37

P/BV: 0,85

Float/Share: $1166

Market Cap: $12,5B

Net Debt: $6,3B

Fairfax Financial Holdings (FFH) is a holding company composed of multiple businesses involved in insurance, reinsurance, restaurants, retail, financial services, industrial, media, and other industries as well. During FFH’s debut in the ’80s, the business was generally perceived as generating very good investment returns coupled with weak insurance operations profitability. Accordingly, FFH had an average combined ratio of 106,7% but a book value compounding at 57.7% on an annual basis from 1985 to 1990. That same story of good returns and weak combined ratio went on until the mid-2000’s when the tendency reversed. From the GFC until now, the combined ratio has been on a downward hill and recorded a 95% annual figure in 2021. Unfortunately, it was now the investment side that was languishing due to Prem Watsa’s bearish stance, and the stock has been suffering from this episode ever since considering it still trading at the same price level as in 2015.

However, there are now good reasons to think that good investment performance is coming back and because FFH never got the chance of coupling good underwriting results with good investment results, investors seem to severely underestimate the true cash generation ability and financial performance of FFH as it exists today. Consequently, this thesis revolves around why I think both the insurance operations and the investment side of the business are now poised to be very rewarding for shareholders in the years ahead.

Insurance Operations

Fairfax's principal insurance subsidiaries are as follow:

- Northbridge, based in Toronto, is one of the largest commercial property and casualty insurers in Canada based on gross premiums written. In 2021, Northbridge’s net premiums written were $1,9B million and the business is responsible for approximately 9% of FFH’s 2021 total gross premiums written($23.8B). It also earned a combined ratio of only 88% in 2021 despite growing its gross premium by 23%.

- The Odyssey Group is based in Connecticut and underwrites treaty and facultative reinsurance and specialty insurance, with principal locations in the United States, Toronto, London, Paris, Singapore, and Latin America. In 2021, Odyssey Group’s net premiums written were $4,85B, representing a year-over-year increase of 29%. Odyssey accounted for approximately 22% of 2021 FFH’s total gross premiums written and FFH owns 90% of the business. It also ended the year with a 98% combined ratio, including a 10% loss related to catastrophes.

- Crum & Forster, based in New Jersey, is a national commercial property and casualty insurance company writing a broad range of commercial, principally specialty, coverages. In 2021, Crum & Forster’s net premiums written were US$2,69B and at year-end, the company had a statutory surplus of $1,85B. The business also accounts for approximately 16% of 2021 total gross premiums written.

- Zenith National, based in California, writes workers’ compensation insurance in the United States. In 2021, Zenith National’s net premiums written were $713M. At year-end, the company had a statutory surplus of $708M. Zenith accounts for approximately 3% of gross premiums written and earned a great combined ratio of only 89% in 2021.

- Based in England, Brit Insurance is a specialty insurer and reinsurer acquired by Fairfax in 2015 and represents approximately 14% of 2021 gross premiums written. Brit did $1,998B in net premiums written during the year, had shareholders’ equity of $1,9B and FFH owns 86% of the business.

- Allied World, based in Bermuda, is 71% owned by FFH and by provides property, casualty, and specialty insurance and reinsurance globally. FFH acquired the stake in Allied during 2017 at a $4.9B valuation when it had a written premium base of $3B. In 2021, premium have now almost doubled with $5.8B and the company is now FFH’s largest insurance company. Allied World represents approximately 24% of 2021 total gross premiums written and generated $3,9B in net premiums written from a 93% combined ratio. As a result, Allied World finished the year with an underwriting profit of $226M and a 25% growth rate in gross premiums.

The balance of Fairfax's insurance operation includes Fairfax Asia, operations in Latin America, Europe, and Fairfax's run-off operations. In 2021, Fairfax Asia grew by 27% and generated $20M in underwriting profits from a 92% combined ratio. The three other regions combined represented ~11% of the consolidated insurances operations’ gross premium during 2021. Overall, 75% of FFH’s business is in North America with the remaining being globally diversified.

Recent Developments in Fairfax Insurance Subsidiaries

The Odyssey Group

In November 2021, FFH announced that it sold a 9,99% stake in Odyssey Group for $900M to two long term business partners, the Canada Pension Plan Investment Board and OMERS. That’s a market value of $9B for a business that FFH was recording on its balance sheet at a $4,9B valuation before the transaction. Besides, the deal was done at 1,84x book value when FFH currently trades around 0,85x book value. Finally, not only does the deal shows how much the book value can be different from the market value, but FFH used the sale proceeds to buy back $1 billion of its own shares at a 0.8x book value multiple. That’s 8% of the shares outstanding.

Allied World

With the Odyssey Group transaction and taking into account the fact that it is not even the biggest insurance company FFH owns, things look especially great for Allied World’s market value. Allied World made $226M in underwriting profits in 2021 fueled by 93% combined profits compared to $92M and a 98% combined ratio for Odyssey Group. However, Odyssey Group had the bulk of the catastrophe-related losses in 2021 with the Hurricane Ida, European floods, and U.S. winter storms. In 2020, both subsidiaries had a much more equal footing with both businesses recording a 95% combined ratio, and $126M in underwriting profits for Allied compared to $190M for Odyssey. From a longer-term perspective, Odyssey Group has a better track record in terms but nonetheless, I think it is fair that say that Allied World is clearly not worth only a half of Odyssey despite being recorded on the balance sheet at $4,8B. Besides, it is good to keep in mind that FFH only trades at a $12,5B market capitalization…

Digit Insurance

As part of Fairfax’s international operation is a 74% owned Indian-based insurance company called Digit. To describe the business in the simplest way possible, it works pretty much like Lemonade in the US does but in India. In other words, Digit is looking to modernize the insurance industry by integrating technologies to process claims. It is, however, much more successful than its US peer with an expected 50% annual increase in gross premium to pass the $700M mark for the year that just ended. It also had a much more reasonable combined ratio of 114% during the year. In addition, India is one of the world’s fastest-growing markets with a population 4 times bigger than in the US. Furthermore, Indians are much more mobile phone-oriented and this should help FFH’s ambition which is for Digit to generate $5B in gross written premium over the medium/long term. That’s truly incredible for a business that was still just a start-up five years ago.

Even more interesting is that before entering into an agreement with certain investors to raise approximately $200M in equity during 2021, Digit was valued at $900M on FFH’s balance sheet. The equity raised was made at a $3,5B valuation which resulted in Fairfax recording a net unrealized gain of $1,49B or $53 of additional book value per share on its investment in Digit. Additionally, Fairfax’s equity accounted interest in Digit will increase by approximately another $0,4 billion, or $14 in book value per share, once the Indian government gives final approval of its announced intention to increase foreign ownership limits in the insurance sector. That new rule will be permitting Fairfax to increase its equity interest in Digit above 49.0% to controlling interest and thereby consolidating the 74% ownership it owns through convertibles on its balance sheet.

Capitalization

FFH finished 2021 with $1,4B in cash and marketable investment at the holding company level even after spending $1B on buybacks following the Odyssey transaction. Going forward, the company recently expressed the desire to keep a similar amount of cash at the holding level in order to sleep comfortably at night no matter what happens.

Concerning the debt to capital ratio, it was lowered to 24.1% from 29,7% in 2021 and represents “close to the lowest levels in the last ten years and [is expected] to decrease in the years to come”. Likewise, their bank lines are fully paid off and there are no significant amounts of debt coming at maturity until 2024. In terms of reserves, FFH reserves level is very strong and had been fueled by favourable reserve developments during the last few years. The table below shows the average annual reserve redundancies for the business it owns for more than a decade.

Float

Over the last ten years, FFH float was not only free of charge, but it also provided a benefit averaging 2,1% a year. By the end of 2021, FFH controlled more than $27,84B in float, which is arguably huge for a 12,5B business. That’s 1166$ of float per share compared to a 550$ share price. With the combined ratio consistently improving in the last years, it might be important to highlight that “every 1% additional benefit would provide approximately $280 million of income, or $12 pre-tax per share”. Even if the combined ratio stopped improving as it can’t go down forever, many millions in income can also be brought by the growing size of the float and gross premium written. On a per-share basis, the float has increased by 10% per year in the last 5 years and by 19% per year since inception.

Operating performance

In 2021, Fairfax reported record performance on nearly every key metric:

1- FFH’s total annual gross premium was up 25.4%, or $4,8B, to $23,8B and up 32% in the fourth quarter. That growth has essentially all been made organically and is a historic record for the company.

2- The combined ratio was significantly down from an average of ~98% during the last decades to a 95% ratio for the whole year 2021 and 88.1% during Q4.

3- With these good results, FFH made $801M in underwriting profit despite absorbing $1.1B in catastrophe losses during the year.

Surely, the current hard market conditions of the last few years helped, but in my opinion, these results could also be pointing toward a bright future for a few reasons. First, if one considers the lag between the moment premiums are written and the moment when they are earned, these underwriting improvements could very possibly be the first of many more to come. In fact, this hard market has not even ended yet. The current inflation could potentially influence juries into awarding higher amounts to claimants and consequently, hurt the weaker carriers. Additionally, the current rising interest rates environment also affects the underwriting ability of the weakly capitalized industry players as their bonds portfolios take a dive. Rightfully for Fairfax, you will see in the next sections how its financial strength and bonds portfolio might end up being very beneficial for the company.

Fairfax also spent years building a global insurance platform and creating a prudent underwriting culture with many of the insurance companies’ managers being with the company for at least 20 years. As such, it seems fair to expect some stability in the aggressiveness or quality of the underwriting activities. In addition, management also took the decision in recent years to restrain itself from making material acquisitions and to let the youngest operations evolve into more mature entities.

Besides, despite FFH’s first 20 years of relatively bad underwriting performance that basically shape the way most investors still perceived the company today, FFH made an underwriting profit in 9 out of the past 10 years. For what it is worth, the combined ratio for FFH in 2022 and 2023 based on the S&P Global rating is now projected to be between 93% and 96%. That is better than the 94-97% ratio that was projected and attained in 2021. S&P Global Ratings also rated FFH with an 'A-' for its core operating companies’ long-term financial strength and issuer credit ratings.

To put that performance into perspective, at a 94% ratio and simply by assuming that net premiums stay at 2021 level ($18,28B), we would see FFH underwriting profits topping $1,1B this year. That’s not considering any growth in net premium written even after decades of continuous growth, including a 26% increase just in 2021 and 23% since inception on a per-share basis.

“Outside North America and Europe, the insurance markets are very underpenetrated and in the future we expect significant growth from our companies there”

In my opinion, the company’s compounding ability is currently overlooked by the market and it definitively has to do with what happened between 2010 and 2017. During these 7 long years, the hedging losses of the investing segment caused the book value to stay essentially flat after paying the dividends despite the gross premium per share increasing 59% from $255 to $405. In other words, the insurance operations got much bigger, and more profitable, without the balance sheet and the investors ever truly noticing.

Bond Portfolio Investments

One of the reasons why insurance companies, in general, are relatively cheap is because they have been suffering from the many years of low-interest rates. However, rates are now rising as nothing last forever and as shown below, FFH is particularly well-positioned for the recent uptrend in yields.

"On December 31, 2021, the company’s insurance and reinsurance companies held $24.9 billion in cash and short-dated investments, representing 50.3% of the portfolio investment. With every 100 bps increase in interest rates, they have already gone up 30 basis points this would provide us with an additional $250 million of additional investment income."

Also, FFH fixed income investments which represent 72% of the total portfolio had a very short duration of only 1.2 years on December 31st, 2021. Almost all competitors have portfolio duration well over 3 years after somewhat “reaching for yields” in the last few years. Not surprisingly, the current uptrend in yields is hurting competitors’ bond value much more and is thereby limiting their ability to aggressively write new premiums. Considering how insurance products are commodity-like, it is very hard to do something different from your competitors. That’s why FFH’s ability to be in the market when others can’t be is truly promising.

“On average we are writing at about 1.0 times net premiums written to surplus. In the hard markets of 2002 – 2005 we wrote, on average, at 1.5 times. As you know, our strategy during times when rates are rising, as they are currently, is to expand significantly in areas where margins are high”

Moreover, it is hard to say exactly how much FFH is going to cash in from interest income given how interest rates are currently volatile, the fact that we can’t predict how much they will buy, and how much they will be able to roll over in the next year. Still, considering that FFH’s 2020 interest income was $716M and only $568M during 2021, we could probably see that number passing the billion-dollar level within one or two years as more cash is invested at higher interest rates.

Equity Investments

Fairfax earned an average return on its overall investment portfolio of ~8,2% since 1985 and 9,2% in 2021. The most successful part of the 36 years track record was definitively in the first two decades. Since 2010, many might not be surprised by the fact that performance was poor, and the main reason being Prem Watsa’s bearish stance. Accordingly, after the GFC when he successfully betted on the crash and made billions from it, Prem’s strategy to stay bearish during the longest bull market in recorded history definitively has had negative effects on FFH. Between 2014 and 2020, FFH lost on average $450M per year from betting on things like BlackBerry, Greece, inflation hedges, market shorts, and greenfield African consumer banks. Therefore, FFH’s book value struggled to compound at a tiny 5% rate over the last decades, even with the tailwinds coming from FFH’s newly profitable insurance operations and relatively good bond portfolio investments despite the low rates environment. Fortunately, in 2019 Prem started being very vocal about FFH mentality change and exited all short investments and the like by early 2020. They also told investors that they would never go down that road again. Only long investment going forward, and the investment portfolio grew by 36% since then.

Considering how Prem Watsa has been successful with his long investment in the past, especially from 1985 to 2000 when FFH book value per share compounded at a 37% annual rate, I think that it is fair to say that if “he walks the talk”, we have a capital allocator of quality aboard. Moreover, I don’t think he lost his touch simply because during the last decade, he deviated from the strategy that made him successful and rightfully admitted that it was a mistake. If he gets back to what has been working for him during his outstanding 36 years track record, I am very comfortable investing in his ability to do just that.

With 2021 now in the rear mirror, Fairfax had a marvellous year with $51,576B in portfolio assets after earning a total of $4,4B during the year. Included in this figure is the $1,4B gain from Digit, the $2,3B in net gains from common stocks, the $641M in interest and dividend income as well as the $402M in FFH’s share of profits of associates. You probably guessed it, the portfolio is heavily weighted in cyclical, industrial, and “deep value” investments that are currently the darling of the equity markets. Still, these types of stocks can turn out to be solid investments if “value stocks” make their comeback against the “growth stocks” popularity of the last decade. Lastly, before thinking that it will still not last, there are a few other things about the FFH’s portfolio strategy that are worth mentioning.

First, Fairfax definitively increased its focus on the quality of the businesses it invests in. FFH somewhat built a reputation for investing in private equity-alike turnarounds that looked statistically cheap. However, the company methodically got out of many weak investments in the last few years. To list quite a few examples; AGT was bought out and taken private, Mosaic Capital went private too, Toys R Us retail business was sold and FFH only kept the real estate, Fairfax Africa was merged with Helios, and EXCO Resources was finally written down and taken private too. Turnarounds can be good opportunities for active investors, but a decentralized structure like FFH wants to own equities, not run them. It was just not their game and they realized it.

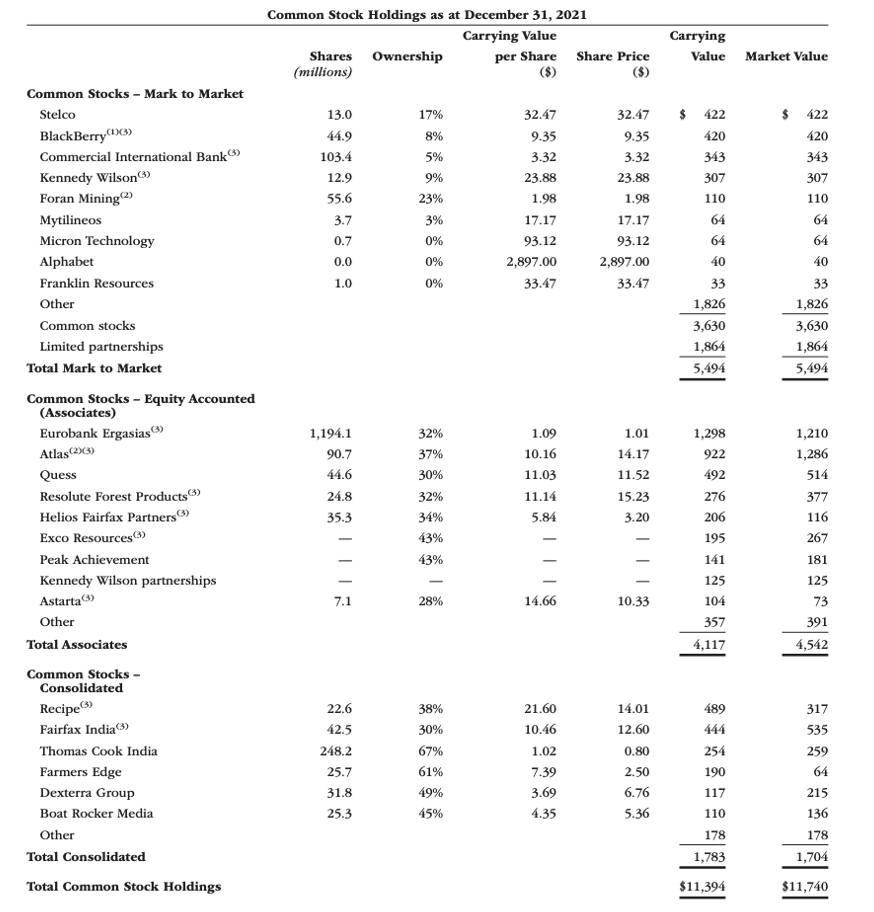

Secondly, as you can see below, FFH’s $11,7 billion equity investment is not only involved in cyclical industries with investment in the banking industry (Eurobank and CIB), the restaurant industry (Recipe), and other things like the media industry (Boat Rocker Media). Not listed below but included in the portfolio are stakes in The Keg, Alibaba, Tencent, and many others that have nothing to do with cyclicals.

As shown above, the company’s common stock holdings’ market value is exceeding the carrying value by $346M. Despite the associated volatility, it is still another 15$ in book value per share hiding in plain sight. Also, among the significant and interesting holdings listed above, let’s dig into some stories highlighting the potential and depth of the current portfolio.

Atlas Corp, which is led by David Sokol and Bing Chen, has been a real investment success for FFH. Since the time he was at Berkshire, David has always been known for his talent as a capital allocator and he is once again proving it with Atlas. The company targets “long-term, risk-adjusted returns across high-quality infrastructure assets in the maritime sector, energy sector and other infrastructure verticals”. With Atlas’s Seaspan containership leasing subsidiary, the company currently operates a 1million TEU capacity which is expected to double in the next few years. The business already got over $12B in gross contracted cash flows and the conservative management team is expecting the company to generate around 2,5$ in earnings per share by 2024, up from the current 1,68$ per share. In addition, FFH just announced its intention to exercise warrants to buy another 25M shares of Atlas at an exercise price of 8,05$ for a total consideration of $205M, bringing FFH ownership to 45,1% of the business. At around 13$ per share, ATCO shares are offering a significant upside for FFH when you consider the soon-to-be realized gains on warrants, the potential upside from the company’s potential, and the fact that Fairfax still holds warrants on another 6M shares.

For Kennedy Wilson, a real estate investment company, led by its founder and CEO Bill McMorrow, has been incredibly rewarding too. In fact, FFH invested a total of $1,15B in the business since 2010 and already received $1,07B in cash proceeds. Fairfax still owns $542M in real estate and 9% of the business. Indeed, the 20% annualized realized return on completed projects might be one of the reasons why at the end of 2021, FFH also committed to providing $1,44B in mortgage loans for an average yield of 4.7% and maturities averaging under 2 years. In February 2022, FFH also “committed to invest $300 million in a 4.75% perpetual preferred in Kennedy Wilson, with seven-year warrants exercisable at $23 per share”. The good news is that KW’s shares are already trading at $24.

Next, another great manager under the FFH umbrella is Stelco CEO, Alan Kestenbaum. The man is an outstanding manager with over $300M in ownership of which he didn’t sell a single share in 2021 even as Stelco’s shares skyrocketed. The high steel prices combined with Stelco’s low-cost position have been very rewarding for the business as it generated free cash flows of over $1,4B and an EBITDA of $2,1B in 2021 alone. With that cash, Stelco raised its dividends twice in 2021 and repurchased 13% of its shares outstanding at a 34,9$ share price, lower than the current 50$ share price. They then repurchased another 5.7% of their shares in January 2022, resulting in FFH ownership increasing from 13,7% to 17,8%. Moreover, Stelco still finished 2021 with over $700M in net cash and is currently trading at a $3,5B valuation, implying more upside than downside in my opinion, even if steel prices can be very volatile.

Likewise, the $1,3B investment in Eurobank might start paying off as the company in which FFH bought a 32,4% stake at an average price of around 0.80 euros in 2019 is already up by over $200M so far in 2022. With the COVID pandemic dissipating and the fact that Greece’s economy is built on tourism and real estate, Eurobank has real chances to be materially beneficial for Fairfax shareholders in the coming years. Since December 31, 2021, Eurobank shares have increased to a high of 1,14 euros per share but are still a far cry from the company book value of 1,47 euros per share. In addition, Eurobank will start paying dividends again for the first time since May 2008 once it obtains regulatory approval to do so in the near future.

Total return swaps (TRS)

Another very good investment made by FFH recently has been its total return swaps. On December 31, 2021, there were swaps outstanding on 1,964,155 Fairfax subordinate voting shares with an original notional amount of $732,5M or approximately $373 per share. With FFH shares priced at $492 on December 31st and at around 550$ in April, the company already recorded net realized gains on investments of $243M. Furthermore, these swaps are still there, and Prem Watsa is very optimistic about them.

“For our stock price to match our book value’s compound rate of 18.2%, our stock price in Canadian dollars should be $1,335(~1000USD). And our intrinsic value exceeds book value, a principal reason being that our insurance companies generate huge amounts of float at no cost. This is the reason we continue to hold total return swaps with respect to 1.96 million subordinate voting shares of Fairfax with a total market value of $968 million at year-end.”

Agreed, some investments have been much less successful like Farmers Edge in agriculture technology, or FFH’s restaurant investments in Recipe or The Keg as they have been severely hurt during Covid. There are also investments that in my mind should just be sold and forgotten, like Blackberry. Still, these companies are either small in proportion to FFH’s total investment portfolio or trading at a substantial discount to their book value. In the case of Blackberry, it remains a $4,4B company that recently sold patents for $600M, increasing its net cash position to just under $1B. Blackberry is also operating in cyber security and embedded operating systems for the automotive industry, two high-growth markets that could surprise many of us. Therefore, it might only be a matter of opinion. Moreover, because Prem is still on the company’s board, there are good chances that he got better insights about the investment than many of us.

Overall, I think that FFH has an interesting and atypical portfolio that can be very profitable in the years ahead. I also think that in less than a decade from now, it is not that far a stretch to build a case in which the combined investment in businesses like Atco, Eurobank, and Digit ends up being worth FFH’s current market cap. Digit has already been a multi-billion gain for Fairfax on the insurance side of its investments and considering how the business is growing, that gain is definitively the first one but might not be the last.

Share buybacks

If you agree with me that FFH is cheap, I think you will also agree with me that buying back shares is a smart thing to do right now. Even more so when you have total return swaps waiting for you to push the stock price higher.

“We'll continue to buy back stocks. I mean we can't control the price of our stock. I said it's ridiculously cheap 2 years ago, said it again, and then we bought 2 million shares.”

-Prem Watsa

Yet, Fairfax’s strategy regarding share buyback goes far beyond being opportunistic at a time when the stock market is looking elsewhere. Going back to the company’s 2018 annual letter, Prem Watsa wrote about how he admired Henry Singleton of Teledyne, who famously retired 90% of Teledyne stock and generated a 3,000% return for shareholders during that same period. Since that 2018 annual letter, Prem talked many times about his desire to do the same type of long-term reduction with FFH shares. Agreed, FFH is still far from matching Teledyne’s accomplishment but an 11% share reduction in 2 years is not a bad start!

Management

On the management side, FFH is truly decentralized with each of its insurance companies operating on a stand-alone basis except when it comes to investment decisions. The investments are made by Hamblin Watsa Investment Counsel which is a wholly-owned subsidiary of FFH that “emphasizes a conservative value investment philosophy, seeking to invest assets on a total return basis including realized and unrealized gains over the long term”.

It is for these reasons that Fairfax is known by many as the “Berkshire Hathaway of Canada”. Other similarities with BRK are FFH’s friendly acquisition strategy, long-term ownership commitment, transparency, humility, and the adherence to value investing core principles. However, investments at FFH have been much more oriented towards real assets, cyclical, and “deep-value” plays whereas BRK is much more about premium quality businesses. It is also very difficult to truly compare both given the differences in size between the two companies and the weight of their insurance operations relative to the overall size of each conglomerate.

Likewise, a very interesting fact about FFH has been said during one of Prem Watsa’s speeches in 2017. What Prem said was that in the company then 31 years of history, he never lost even one of his managers to another company despite others sometimes offering better compensation packages. That’s also why most of the subsidiaries and affiliates’ managers have more than 20 years of working history at the company. Prem is also one of the (too) few managers in the corporate world to have achieved the long-term target he publicly set for his company. In fact, since 1985, FFH’s stated objective has always been to build long-term shareholder value by compounding book value per basic share over the long term by 15% annually.

“Over our 36 years, excluding dividends, we have compounded book value by 18.2% annually and our stock price has compounded by 15.7% annually. Over these 36 years, there are only 67 companies of the 6,000 companies listed in 1985 on the U.S. exchanges (NYSE, NASDAQ and American) – i.e. only 1% – that have had an annual return above 15%.”

As discussed earlier, it is not to say that everything Prem made was perfect, but I think that Prem still succeeded in strengthening the fundamentals of the business in recent years, especially on the insurance side. It is for this reason that the future looks much brighter than the company’s current market valuation suggests. Prem could not agree more considering that he personally acquired an additional $150M stake in FFH during the summer of 2020. With over a billion-dollar ownership, I am ready to assume that he is still very motivated to make FFH great again.

“At our AGM and on our first quarter earnings release call, I said that our shares are ‘ridiculously cheap’. That statement reflected my recognition that in the 35 years since Fairfax began, I have never seen Fairfax shares sell at a bigger discount to their intrinsic value than they have recently. I have now backed up my strong words by purchasing close to US$150 million of Fairfax shares in the market over the last few days, as I believe that this will be an excellent long-term investment.”

Valuation

Before crunching the numbers and discussing the potential returns, it is important to consider how the share price has been flat despite key metrics significantly strengthening in the last years.

Agreed, book value valuation should ultimately be more accurate and will be presented below. However, I thought it would be interesting to show you that this investment isn’t just a “value trap” with good-looking assets but poor prospect.

About my assumptions

Net Premium Earned: Given that the net premiums earned in 2021 were $18,28B, I used it as my pessimistic case. Considering the current hard market, FFH’s underwriting strategy and historical growth rate of 23% on a per-share basis since inception and 26% during 2021. I still chose to not extrapolate that performance as 26% is outside of what you can expect from a company of that size in the P&C industry. So, I kept my growth rate between 0% and 15%.

A 95% Combined Ratio; due to the 88% ratio attained in Q4 and the annual 95% for 2021 despite $1,1B in catastrophe losses; the S&P ratings; FFH operations maturing; and the current hard market.

Investment Portfolio Assets Growth: Historically, the float has grown by 19% on an average annual basis as the premium grew around that same pace too. Therefore, I used the same growth rate in the investment portfolio as I used for the growth in net premiums. That’s a bit imprecise given that it will also depend on the investment performance but as John Maynard Keynes famously said; “it is better to be roughly right than precisely wrong”.

Rate of Return on Investments: I used return rates from 5% to 10% as historically, Prem has been able to earn returns ranging from 2.3% and 11% based on 5-year periods since 1985. I expect Prem to do better than the 2.3% he earned between 2011 and 2016 as he learned from his mistakes and has been earning 5.7% on average since 2017 and 9.2% in 2021. Since inception, FFH earned close to 8.2% on its investment. It is also based on his current bonds and equity positions that we talked about in detail earlier.

Interest Expense: I decided to push down the interest cost because FFH debt is about $1B lighter than what it used to be at the start of 2021 (7,8B vs 8,8B) and that the interest rate of its debt is lower than in 2020 because FFH repaid $670M in debt yielding on average 5,23% and reissued $600M at 3,375% maturing in 2031. They also incurred a $45,7M loss on the redemption of the debt they repaid. So, 475M compared to the $517M that it cost them in 2021 looks very fair to me.

Corporate Expense: I used $575M as a pure “guesstimate” as it seems to follow the $35-40M annual increase of the last years and the fact that there are no real changes regarding acquisitions or the like.

Income tax rate: Simply the Canadian tax rate.

Dividends on preferred stocks: Their preferred stocks are only redeemable in 2024 and 2025 and there was no issuance in 2021 so I used the same number as last year.

Income Attributed to Minority Interest: That’s another very honest “guesstimate” considering that there are many businesses in many industries and with many different ownership situations. I also wanted to reflect the growth I anticipate for the businesses a whole and as such, I pushed the number up to $300M from $192M in 2021.

Shares outstanding: I went with 23.9M for the pessimistic case, meaning that share counts would stay the same. That’s my pessimistic case because I surely don’t expect FFH to issue new shares and with all they’ve done recently in addition to how cheap the stock is right now; it would be surprising that they do not buy back more stocks. For the Optimistic case, I went with almost 2M in buybacks as it is what they did this year. However, with the price going higher and their will to keep the balance sheet very strong, it would be surprising, but not impossible, to see the management going after more than 2M shares.

P/E Multiple: Due to FFH earnings are very lumpy due to the various way it earns its profits and because financials are generally trading at low multiples to earnings, I decided to go with a P/E range from 5 to 13. In my opinion, it looks very reasonable on an absolute basis and on a comparative basis as Markel, Berkshire, Alleghany trade between 11x and 25x NTM earnings. On a more speculative touch, it would also not be surprising to see the whole insurance sector becoming much more appreciated by the investing community after the initial losses of insurers bonds portfolio and therefore, potential upgrades and multiple expansions could be underway.

Share Price Expectation: With the share price trading at 550$, I think the results speak for themselves. At a P/E ratio of 7, no premium growth, with same investment portfolio size earning only 5% even with interest income definitively going up in the next few years, and no share buybacks, FFH would trade at around 425$. That looks like a small downside risk to me.

On the other side, at a P/E of only 10, a 10% increase in premium written, a 10% in investment portfolio assets growth earning a 7.5% return and 50% less in buybacks than last year, the stock has a 120% upside (1200$).

Finally, with a P/E of 13, a 15% growth in premium written (which is smaller than last year’s 26% growth), a 15% growth in portfolio investment assets earning a 10% return, and the same amount they did in buyback as they did in 2021, FFH would trade around 2380$. That’s an upside of ~333%.

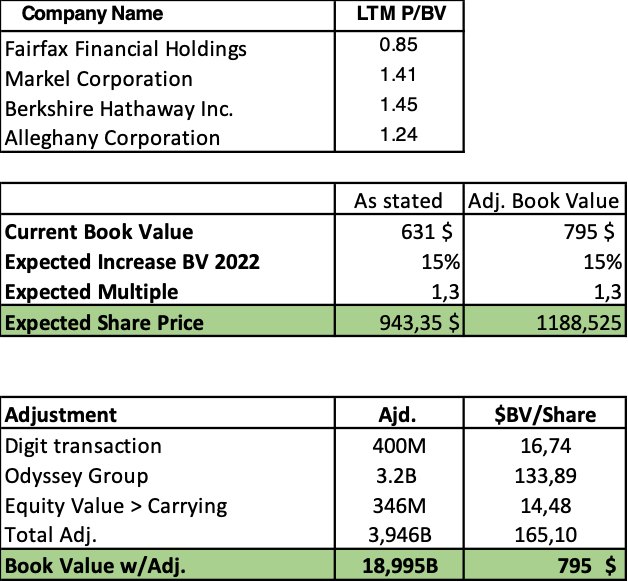

Book Value Valuation

“For our stock price to match our book value’s compound rate of 18.2%, our stock price in Canadian dollars should be $1,335. And our intrinsic value exceeds book value, a principal reason being that our insurance companies generate huge amounts of float at no cost.”

For the book value valuation, I decided to give FFH a 1.3x multiple as the company has historically traded most of the time between 1.1x and 1.4x but also because it was in line with line other players’ valuation. It is also important to consider that because FFH insurance operations have grown despite the book value barely increasing between 2010 and 2017, the book value of FFH is much less representative of the intrinsic value compared to competitors’ book value. In other words, FFH has been the equivalent of a high earner but big spender. The company’s wealth is much smaller than if it had been saving instead of spending. However, on a forward-looking basis, it has pretty much the same abilities to earn and save. That’s why the balance sheet is not representative of what people are ready to pay to acquire the assets’ future cash flows and that’s why Odyssey Group sold at a $9B valuation or 1,84x BV. The nice thing is that it is applicable for all insurance and reinsurance subsidiaries that have been on the balance sheet since Prem’s bearish episode and as such, the 1,3x multiple might be very conservative. Conjointly, I decided to only adjust the book value with the elements which are based on actual facts. For Odyssey it is the $9B transaction, for Digit it’s the gains awaiting to be recorded once the Indian government gives its regulatory approval, and the last adjustment is based on the investment portfolio market value in excess of book value as of December 31st, 2021.

Conclusion

To Conclude, with an estimated business value averaging close to 1200$ on a book value and earning multiple valuations, the $550 share price looks especially interesting for the shareholders. Given that FFH is controlled by a capital allocator of quality, that the financials are sound, and that the price is offering one hell of a margin of safety, I think that this opportunity is especially interesting on a risk/return basis.

Insightful Article! Thanks for sharing this, appreciate your time and effort!!!